Acquiring vs QR Payments in Ukraine: Complete Comparison Guide 2025

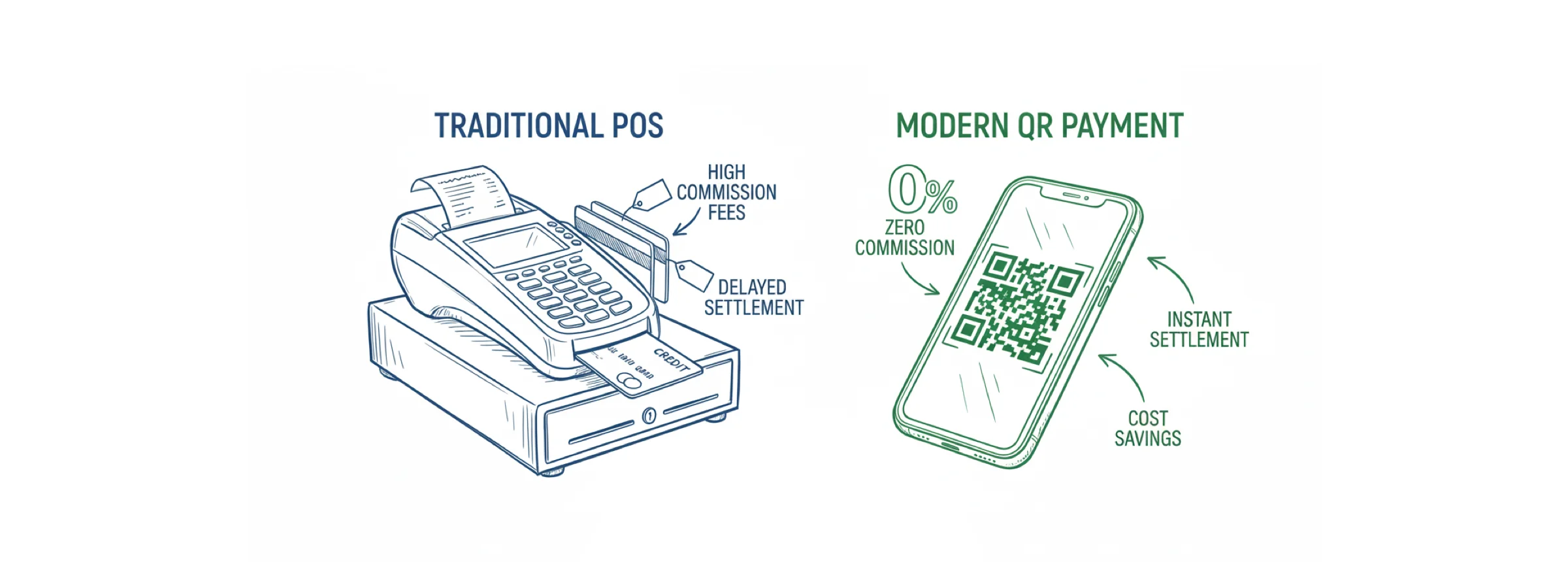

QR payments via IBAN transfers are revolutionizing Ukrainian small business payments — they allow merchants to accept payments with zero commission while receiving funds instantly. While traditional acquiring costs businesses 1.3% to 2.75% per transaction plus monthly fees, IBAN-based QR payments eliminate these costs entirely. According to the NBU, 94.6% of all card transactions in Ukraine were cashless in 2024, and the market continues to grow rapidly.

This article helps entrepreneurs choose the optimal payment acceptance method: from classic POS terminals to innovative solutions like pmnt.app, which generates QR codes for commission-free IBAN transfers.

Traditional merchant acquiring: equipment, fees, and hidden costs

Merchant acquiring remains the most common way to accept card payments in Ukraine — 518,400 retail locations are equipped with POS terminals as of late 2024. However, convenience comes at a price: total cost of ownership can reach UAH 8,000–15,000 per year for small businesses.

Base rates from leading banks

PrivatBank offers 1.3% commission per transaction with a monthly fee of UAH 400. The bank provides a free modern Android terminal supporting NFC, Apple Pay, and Google Pay. Setup takes up to 36 hours, and funds are credited the next business day. An integrated software cash register (PRRO) is included.

PUMB has set commission at 1.2% (promotional offer until January 5, 2026) with a base rate of UAH 0 for new clients for the first 6 months. The standard rate is 1.3% with a monthly fee of UAH 300. Funds are credited daily by 6:00 AM, including weekends. The bank offers mobile and stationary terminals from Castles, Verifone, and Ingenico.

Monobank charges 1.3% for Ukrainian card transactions and 2% for foreign cards, with a monthly fee of UAH 500. For restaurants (MCC 5812), the monthly fee may be waived. The bank is known for the fastest setup — just a few hours.

Oschadbank offers 1.3% commission with a monthly fee of UAH 400–500 depending on terminal type. Since April 2024, the bank has significantly reduced rates to support businesses.

Raiffeisen Bank has set commission at 1.5% with a fixed fee of UAH 400/month per retail location. The first month is free for new clients.

Comparison table of merchant acquiring rates

| Bank | Commission (UA cards) | Commission (foreign) | Monthly fee | Settlement |

|---|---|---|---|---|

| PrivatBank | 1.3% | 1.3% | UAH 400/mo | Next day |

| PUMB | 1.2–1.3% | 1.3% | UAH 0–300/mo | Daily by 6 AM |

| Monobank | 1.3% | 2.0% | UAH 500/mo | Next day |

| Oschadbank | 1.3% | 1.3% | UAH 400–500/mo | Next day |

| Raiffeisen | 1.5% | 1.5% | UAH 400/mo | Next day |

| Abank | 1.2% | — | — | Next day |

Additional costs and limitations

Beyond official rates, entrepreneurs face hidden costs. Some banks require a minimum monthly turnover — for example, UKRSIBBANK has set a threshold of UAH 50,000/month. Non-compliance may result in additional charges or contract termination.

Installation restrictions also create inconveniences: PrivatBank prohibits installation in residential premises, temporary structures, and locations without signage. Replacing faulty equipment takes 3 business days, which is critical for business continuity.

Internet acquiring: online payment costs for e-commerce

Internet acquiring serves 13.6% of all cashless transactions with an average receipt of UAH 561. This segment shows the fastest growth — +14.5% compared to 2023.

LiqPay from PrivatBank

LiqPay is the largest market player with over 25,000 active clients. Standard commission is 2.75%, but platform partners (Prom, Rozetka) receive a reduced rate of 1.5%. Utility companies enjoy a preferential rate of 1%, insurance companies and tour operators — from 2.2%.

LiqPay's main advantage is settlement speed: for PrivatBank clients, funds arrive instantly 24/7; for other banks — within 1–3 days. No monthly fee, free setup. Promotional offer with Visa: 0% commission on the first UAH 50,000 turnover for new clients.

PUMB hutko

hutko from PUMB offers 1.5% commission for turnover up to UAH 5 million/month (individual terms for higher volumes). Foreign card commission is calculated separately. Funds are credited daily, including weekends.

A unique feature is support for 200+ countries and 150+ currencies with automatic conversion to hryvnia. The payment page is available in 22 languages. Ready-made modules for Shopify, Wix, and other CMS platforms.

PUMB B2B internet acquiring

For corporate clients, PUMB offers differentiated rates: 1.3% for Ukrainian cards and 2.3% for foreign cards. Funds are credited the next day between 10:00 and 11:00. Guaranteed refund to customer — by the 3rd business day.

Raiffeisen internet acquiring

Raiffeisen Bank has set a single rate of 1.5% for all cards with no monthly fee. Funds arrive immediately after a successful transaction — the fastest settlement among banks. Visa, Mastercard, American Express, and PROSTIR are supported.

Internet acquiring comparison table

| Provider | Commission (UA) | Commission (foreign) | Settlement | Features |

|---|---|---|---|---|

| LiqPay | 1.5–2.75% | 1.5–2.75% | Instant/1–3 days | 25,000+ clients |

| PUMB hutko | 1.5% | Individual | Daily | 200+ countries |

| PUMB B2B | 1.3% | 2.3% | 10:00–11:00 | Corporate |

| Raiffeisen | 1.5% | 1.5% | Instant | American Express |

| Monobank Plata | 1.3% | 2.0% | Next day | Charities |

| Fondy | 1.5%+ | 2.0%+ | 1–2 days | API, SDK |

Tap-to-Phone: smartphone as terminal

Tap-to-Phone technology transforms a regular smartphone into a payment terminal and is becoming a popular alternative for mobile businesses. As of 2024, over 7,000 Oshchad PAY terminals are active in just one bank.

PrivatBank Terminal (Tap to Pay)

The "Terminal" app from PrivatBank supports iOS (iPhone XS+, iOS 16.4+) and Android with NFC. Commission is 1.3% with no monthly fee and no equipment required. Setup is instant, and funds are credited the next day.

Additional features include an integrated PRRO, multi-merchant capability (multiple entrepreneurs through one app), tipping service, and Face ID. Referral program with Visa (until December 31, 2025): UAH 100 for referred friends + UAH 200 bonus for turnover exceeding UAH 8,000 in 60 days.

PUMB Terminal

PUMB Terminal works on Android smartphones with NFC. Commission — 1.3%, no monthly fee. Integration with PRRO: E-check and Checkbox. PCI DSS certificate confirms data processing security.

Tap-to-Phone solutions comparison

| Bank | Commission | Monthly fee | Platforms | PRRO |

|---|---|---|---|---|

| PrivatBank | 1.3% | UAH 0 | iOS, Android | ✓ |

| PUMB | 1.3% | UAH 0 | Android | ✓ |

| Monobank | 1.3% | UAH 0 | iOS, Android | ✓ |

| Oschadbank | 1.3% | UAH 0 | Android | ✓ |

| Raiffeisen | 1.5% | UAH 0 | Android | — |

QR payments and IBAN transfers: a revolution for small business

QR payments via IBAN transfers are the only way to accept cashless payments with zero merchant commission. This fundamentally differentiates them from all types of acquiring, where the merchant always pays a percentage of the transaction amount.

How IBAN QR payment works

When scanning a QR code with IBAN details, the buyer makes a regular bank transfer to the seller's account. Key advantages:

- Merchant commission: 0% — seller receives the full amount

- Buyer commission: according to their bank's rates (usually UAH 0–2 for hryvnia transfers, often free)

- Fund settlement: instant via SEP 4.1 system (up to 10 seconds)

- Equipment: not required

- Monthly fee: none

- Setup: not needed, works with any business account

NBU and QR payment standardization

The National Bank of Ukraine has standardized the QR code format for IBAN transfers. Since December 2024, the SEP 4.1 electronic payment system provides instant settlement — up to 10 seconds 24/7. PrivatBank joined the system on December 12, 2024.

Limitations and limits

According to the Ukrainian Banks Memorandum (44 participating banks), from June 1, 2025, there is a limit of UAH 100,000/month for P2P and IBAN transfers for individuals. For entrepreneurs (FOP) and legal entities, restrictions do not apply to transfers to business accounts.

Exceptions from limits: clients with confirmed income, volunteers, transfers between own accounts, payment for goods and utilities.

Comparative analysis: total cost of ownership per year

Let's examine the real economics for small businesses with different transaction volumes. Assuming an average receipt of UAH 500.

Scenario 1: Micro-business (turnover UAH 50,000/month)

| Solution type | Commission | Monthly fee | Annual cost | Savings vs QR |

|---|---|---|---|---|

| POS terminal 1.3% | UAH 7,800 | UAH 4,800 | UAH 12,600 | −UAH 12,600 |

| Tap-to-Phone 1.3% | UAH 7,800 | UAH 0 | UAH 7,800 | −UAH 7,800 |

| Internet acquiring 1.5% | UAH 9,000 | UAH 0 | UAH 9,000 | −UAH 9,000 |

| QR/IBAN (pmnt.app) | UAH 0 | UAH 0 | UAH 0 | Baseline |

Savings with QR payments: UAH 7,800 to 12,600 per year.

Scenario 2: Small business (turnover UAH 200,000/month)

| Solution type | Commission | Monthly fee | Annual cost | Savings vs QR |

|---|---|---|---|---|

| POS terminal 1.3% | UAH 31,200 | UAH 4,800 | UAH 36,000 | −UAH 36,000 |

| Tap-to-Phone 1.3% | UAH 31,200 | UAH 0 | UAH 31,200 | −UAH 31,200 |

| Internet acquiring 1.5% | UAH 36,000 | UAH 0 | UAH 36,000 | −UAH 36,000 |

| QR/IBAN (pmnt.app) | UAH 0 | UAH 0 | UAH 0 | Baseline |

Savings with QR payments: UAH 31,200 to 36,000 per year.

Scenario 3: Medium business (turnover UAH 500,000/month)

| Solution type | Commission | Monthly fee | Annual cost | Savings vs QR |

|---|---|---|---|---|

| POS terminal 1.3% | UAH 78,000 | UAH 4,800 | UAH 82,800 | −UAH 82,800 |

| Tap-to-Phone 1.3% | UAH 78,000 | UAH 0 | UAH 78,000 | −UAH 78,000 |

| Internet acquiring 1.5% | UAH 90,000 | UAH 0 | UAH 90,000 | −UAH 90,000 |

| QR/IBAN (pmnt.app) | UAH 0 | UAH 0 | UAH 0 | Baseline |

Savings with QR payments: UAH 78,000 to 90,000 per year.

Impact on cash flow: avoiding cash gaps

Settlement speed is a critical factor for small business:

- QR/IBAN: instant (SEP 4.1 — up to 10 seconds)

- Acquiring: 1–3 business days

With daily turnover of UAH 10,000, a 2-day delay means UAH 20,000 in frozen funds. For businesses with high turnover (groceries, HoReCa), this creates a constant cash gap.

Use cases for different business types

Coffee shop or food court

Traditional approach: POS terminal with 1.3% commission + UAH 400/month. With average receipt of UAH 120 and 1,000 transactions per month: 120,000 × 1.3% + 400 = UAH 1,960/month.

QR solution (pmnt.app): Printed QR code near checkout, payment via customer's banking app. Cost: UAH 0. Savings: UAH 23,520/year.

Freelancer or consultant

Traditional approach: LiqPay with 2.75% commission. With income of UAH 30,000/month: UAH 825/month in commission.

QR solution (pmnt.app): Sending QR code to client via messenger or email. Cost: UAH 0. Savings: UAH 9,900/year.

Online store (medium)

Traditional approach: Internet acquiring 1.5% on UAH 500,000/month turnover: UAH 7,500/month.

Hybrid approach: QR payment for 50% of transactions + acquiring for the rest. Savings: UAH 45,000/year.

Market or fair

Traditional approach: Tap-to-Phone 1.3% (if NFC smartphone available) or no cashless option.

QR solution (pmnt.app): Printed QR code without needing a smartphone for the seller. Cost: UAH 0. Works offline — the buyer scans the code with their phone.

pmnt.app advantages for QR code generation

pmnt.app is a free QR code generation service for IBAN payments that fully complies with National Bank of Ukraine standards.

Key features

- Free generation of unlimited QR codes

- NBU standards compliance — QR codes are correctly read by all Ukrainian banking apps

- Compatibility with all Ukrainian banks — PrivatBank, Monobank, Oschadbank, PUMB, Raiffeisen, and all others

- Multiple interfaces: web interface, Telegram bot, API, MCP server

- No fiscal registration required for QR code (fiscalization is done separately via PRRO)

Integration and automation

pmnt.app API allows automatic QR code generation for integration into:

- Invoicing systems

- Online stores

- CRM systems

- Mobile applications

- Telegram bots for business

MCP server provides integration with modern automation tools and AI assistants.

Market trends and cashless payment prospects

Market statistics 2024–2025

According to NBU, the Ukrainian cashless payment market demonstrates rapid growth:

- 132 million payment cards issued (+15% vs 2023)

- 58.8 million active cards (+13%)

- 16.5 million tokenized NFC cards (+33%)

- 496,600 POS terminals (+10.5%)

- 95% of transactions at retail — contactless

Growth of alternative payment methods

The share of card-to-card transfers grew to 31.1% by amount (UAH 1.34 trillion). This indicates growing popularity of P2P and IBAN transfers among businesses.

QR payments are actively implemented by banks: Monobank, PrivatBank, Raiffeisen, and others offer QR checkouts. However, commission remains at acquiring level (1.2–1.5%). IBAN transfers via QR code are the only commission-free option.

Instant payments SEP 4.1

The launch of SEP 4.1 in December 2024 was a turning point for IBAN transfers. Execution time dropped to 10 seconds, making QR payment as fast as card acquiring but without commission.

Conclusions: when to choose acquiring vs QR payments

QR payments via IBAN (pmnt.app) are optimal for:

- Micro and small businesses with turnover up to UAH 500,000/month

- Freelancers and consultants

- Service sector (salons, repairs, tutors)

- Market and fair trade

- Businesses with critical need for instant settlement

- Startups at market testing stage

Traditional acquiring is appropriate for:

- Large retail chains with high service speed requirements

- Businesses with predominantly foreign customers (cards)

- Situations where familiar interface is critical for buyers

- Integration with bank loyalty systems

Hybrid approach

The optimal strategy for most is a hybrid model: QR payment for regular customers and small amounts, acquiring for large transactions and foreigners. This maintains convenience while significantly reducing costs.

pmnt.app provides simple QR payment implementation without technical integration and costs — just generate a code and print it or send it to the customer.