New NBU QR Code Rules for Instant Transfers: What Businesses Need to Know

Starting November 1, 2025, updated regulations for QR code formation, transmission, and processing for credit and instant credit transfers came into effect in Ukraine. These changes, introduced through NBU Resolution No. 97, establish a unified system for QR code payments that promises to simplify cashless transactions and strengthen Ukraine's digital payment infrastructure.

What Changed on November 1, 2025?

The National Bank of Ukraine implemented comprehensive updates to the rules governing QR code structure and graphic representation for payment transfers. These changes affect all payment service providers (banks) operating in Ukraine and introduce new standards for how QR codes are generated, displayed, and processed.

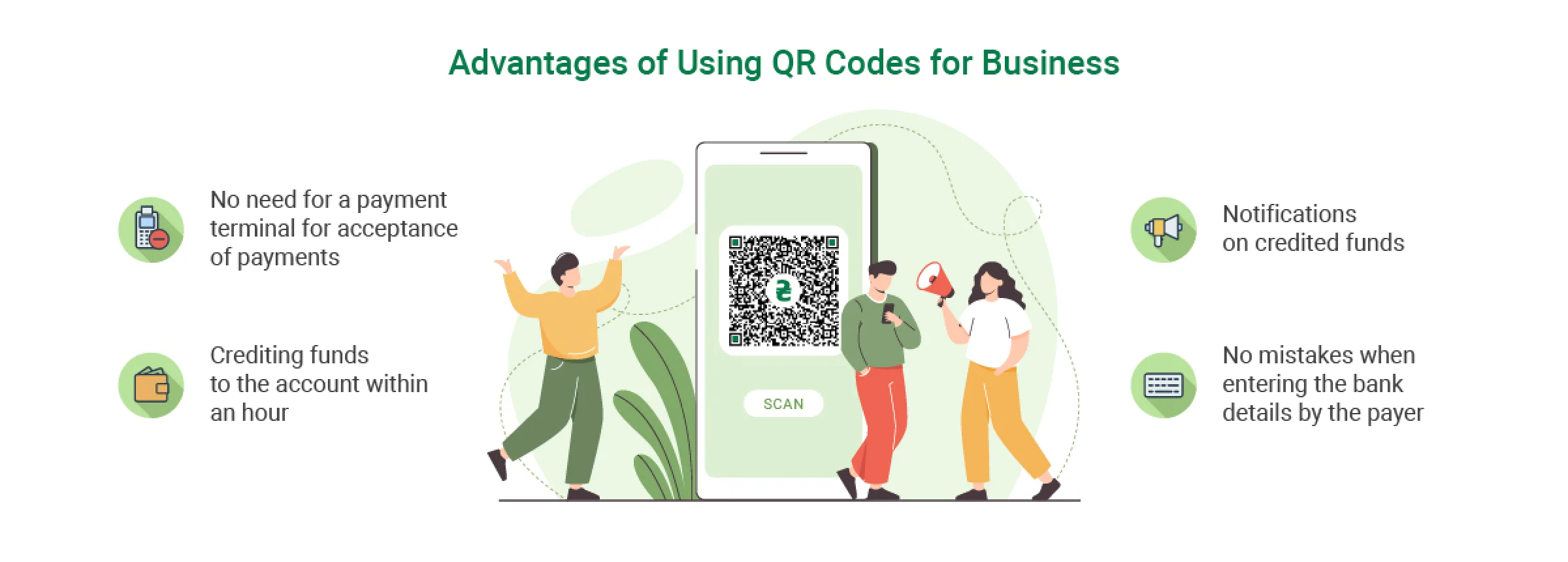

Key Changes at a Glance

The updated regulations introduce several significant improvements to the QR code payment system:

Universal QR Scanner Integration: Every account holder will now have access to a QR code scanner on the initial screen of their banking app, making it easier to initiate payments by scanning codes.

Cross-App QR Code Exchange: Within a single mobile device, users can now generate, display, and exchange QR codes between different banking apps using deeplinks. This functionality is particularly valuable for e-commerce applications and instant payment scenarios.

Enhanced Merchant Integration: QR codes can now transmit merchant-specific identifiers including point-of-sale locations and invoice numbers. This enables automated processing in retail management systems like SAP, streamlining accounting and reconciliation processes.

Field Protection for Merchants: Merchants can now set restrictions that prevent customers from editing certain payment fields. This ensures that customers pay exactly the amount specified by the merchant, reducing errors and disputes.

Technical Specifications

The new regulations establish precise technical requirements for QR code implementation. Payment QR codes must now include all mandatory elements in a clearly defined sequence, with strict adherence to encoding and data volume optimization standards.

QR codes can range from version 10 to 20, with error correction levels of Q, M, or L depending on the amount of information and scanning conditions. The central placement of the hryvnia symbol in a white circle is mandatory for formats 002 and 003, while remaining optional for format 001.

The Instant Payments Ecosystem for Merchants

Beyond QR code standardization, the NBU is developing a comprehensive instant payments ecosystem that offers multiple implementation options for businesses.

Three Pathways for Merchant Integration

Self-Acquiring: Businesses can implement payment acceptance independently without intermediaries, reducing costs and maintaining direct control over transaction processing.

Traditional Acquiring: Merchants can partner with banks for traditional acquiring services, leveraging established infrastructure and support systems.

Open Banking Integration: Through open banking protocols, businesses can access innovative payment solutions that connect directly with customers' banking apps.

Implementation Challenges and Solutions

While the new system offers significant advantages, the NBU has identified several challenges that businesses and payment providers may encounter during the transition period.

Customer Experience Considerations

The payment flow for instant transfers at physical points of sale differs from traditional card payments. The NBU recommends that instant payments are best suited for:

- Physical locations without significant queues

- Self-service checkout systems

- E-commerce channels where Google Pay or Apple Pay buttons are not available

In e-commerce scenarios particularly, instant payments often provide a simpler customer experience compared to card payments when alternative payment methods are absent.

Fee Structure Concerns

Some payment service providers currently charge fees to payers for instant transfers. The NBU continues to work with the industry to establish competitive pricing that encourages adoption while maintaining service sustainability.

Merchant Education and Support

Many merchants remain uncertain about how to organize instant payment acceptance. The NBU has established dedicated support resources and regularly updates guidance materials to help businesses navigate the implementation process.

Looking Ahead: Integration with European Systems

The NBU's roadmap for instant payments extends beyond domestic implementation. Plans include integration with the Single Euro Payments Area (SEPA) instant transfer system, which will enable seamless cross-border payments between Ukraine and EU member states.

This forward-looking approach aligns with Ukraine's broader integration goals and prepares the country's financial infrastructure for EU membership requirements.

What Businesses Should Do Now

For businesses accepting payments in Ukraine, the transition to the new QR code system represents both an opportunity and a responsibility. Here are key action steps:

-

Update Payment Applications: Ensure your banking apps and payment systems are updated to support the new QR code standards.

-

Educate Staff and Customers: Train employees on the new payment flow and prepare customer-facing materials explaining how to use QR code payments.

-

Evaluate Integration Options: Consider which approach—self-acquiring, traditional acquiring, or open banking—best fits your business model.

-

Test Implementation: Conduct thorough testing of QR code generation and scanning functionality before full deployment.

-

Monitor Feedback: Gather customer feedback during the transition period to identify and address any friction points.

Conclusion

The November 1, 2025 implementation of new NBU QR code rules marks a pivotal moment in Ukraine's journey toward a modern, efficient, and European-integrated payment system. While challenges exist, the potential benefits for businesses, consumers, and the broader economy are substantial.

By standardizing QR code payments and establishing clear technical requirements, the NBU has created a foundation for innovation in digital payments. Businesses that embrace these changes early will be well-positioned to offer customers convenient, secure, and cost-effective payment options that align with both domestic needs and international standards.

The success of this initiative depends on collaboration between regulators, payment service providers, merchants, and consumers. As the ecosystem matures, Ukraine's payment infrastructure will become increasingly competitive, transparent, and integrated with European systems—a crucial step in the country's economic development and EU integration journey.